TL;DR: Most EOFY vehicle purchase urgency is manufactured pressure, not tax logic. Car depreciation limit caps at $69,674 for 2025-26. Instant asset write-off is $20,000. Real tax benefits exist only when your marginal rate, business usage, and operational timing align. Trade-ins trigger depreciation recapture that often neutralises June urgency. Your accountant should calculate actual claimable amounts before you act.

Some of this urgency is legitimate. Most of it isn't.

Core Facts:

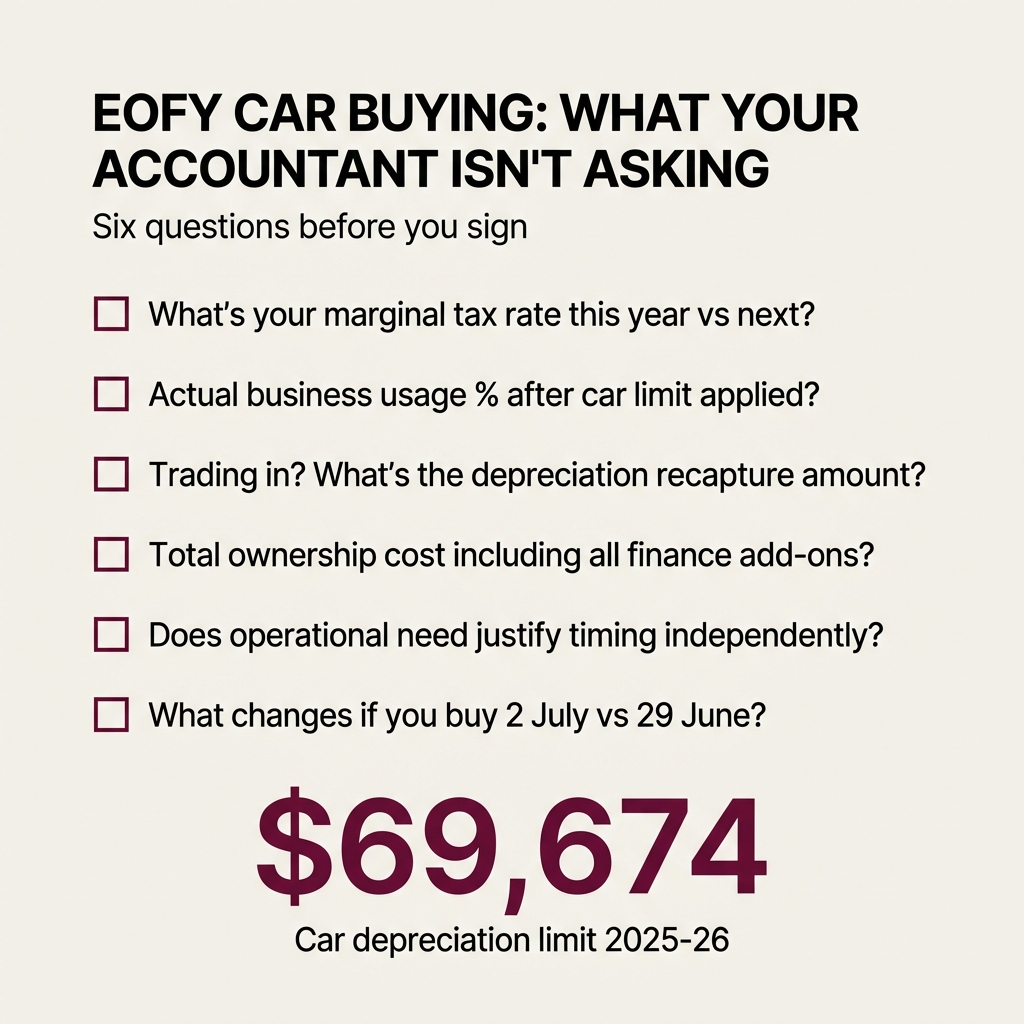

Car depreciation limit for 2025-26: $69,674 (maximum claimable value)

Maximum GST credit: $6,334 (one-eleventh of car limit)

Instant asset write-off: $20,000 (extended to 30 June 2026, now law)

Timing matters only when: higher tax rate this year, genuine operational need, or under $20,000 threshold

Trade-ins create depreciation recapture that appears on same tax return as new deductions

Genuine tax considerations get weaponised into manufactured scarcity. Buyers who could benefit from strategic timing rush into decisions that don't serve them. Buyers with no tax-driven reason to act get swept up in pressure unrelated to their situation.

What actually matters when you're looking at end-of-financial-year vehicle acquisition, and what your accountant should ask before you commit to anything.

What Are the Actual Tax Thresholds for EOFY 2025-26? For the 2025-26 financial year, the car depreciation limit in Australia is $69,674. This is the maximum value you use to calculate depreciation on a vehicle for business purposes, regardless of what you paid.

This creates a constraint: the maximum GST credit claimable is $6,334 (one-eleventh of $69,674). Buy a vehicle above this threshold, and you get no additional tax benefit beyond this point.

The instant asset write-off sits at $20,000 and has been extended to 30 June 2026. This measure is now law. For passenger vehicles, the car limit still applies. Even with the instant write-off, you claim only up to the $69,674 depreciation cap.

The timing dependency is real, but narrow. Tax thresholds apply to vehicles first used or leased in the 2026 income year (1 July 2025 to 30 June 2026). Purchased before 1 July 2025? Previous year's limits apply.

What most dealers won't explain: you depreciate a car only from the date it was first used. Write off the entire amount? You claim the purchase price up to the car limit as a tax deduction for that financial year.

The question your accountant should ask first: Does the timing of this deduction materially change your tax position this year, or are you accelerating a purchase that would deliver the same benefit next financial year?

Key point: Tax thresholds are fixed, but timing benefits depend entirely on your specific marginal rate and operational needs.

How Does the Tax Benefit Calculation Actually Work? Most EOFY sales material presents tax benefits as automatic. They're not. The calculation sequence determines whether you're getting genuine value or theatre.

Here's how the calculation works :

Step 1: Apply the car limit. Purchased a vehicle for $80,000? Maximum claimable amount is $69,674.

Step 2: Calculate business usage. Logbook shows 90% business usage, 10% personal? Maximum you claim is 90% of $69,674, which equals $62,706.60.

Step 3: Determine depreciation method. Choose instant write-off eligibility or depreciation based on vehicle cost and your business structure.

This sequence exposes the gap between what dealers suggest you'll save and what you'll claim. Buying a $90,000 vehicle and assuming you'll get tax benefits on the full amount? You're miscalculating by more than $20,000 before accounting for personal usage.

The question your accountant should ask: What's your actual business usage percentage, and have you calculated the claimable amount based on the car limit before applying that percentage?

Key point: The car limit applies first, then business usage percentage. Most buyers reverse this calculation and overestimate their deduction.

What Happens to Depreciation When You Trade In a Business Vehicle? A structural element ignored during EOFY pressure: trade in a business vehicle, and you recognise the depreciation recapture as taxable income.

The trade-in is treated as a sale at fair market value, followed by a purchase. The depreciation recapture appears as income on your tax return. The new depreciation deductions from your new vehicle offset that income on the same return.

This changes the urgency calculation. The "must buy before 30 June" pressure becomes less significant when the depreciation recapture and new deductions appear on the same tax return, whether you complete the transaction in June or July.

The question your accountant should ask: If you're trading in a depreciated business vehicle, have you calculated the recapture amount and determined whether the timing of this transaction changes your net tax position?

Key point: Trade-ins create offsetting entries on the same tax return, which often eliminates the tax timing advantage dealers claim.

When Does EOFY Timing Actually Benefit You? Scenarios where end-of-financial-year timing creates legitimate advantage exist. They're more specific than dealers suggest.

Genuine cash flow benefit from accelerating the deduction. Your business had a strong year. You're facing a higher marginal tax rate this year than next year. Bringing the deduction forward has measurable value.

Operational need before the new financial year begins. Vehicle is required for business operations starting 1 July. Timing is driven by operational need, not tax theatre.

Below the instant asset write-off threshold. Purchasing a vehicle under $20,000 and claiming the instant write-off based on your business structure? Deduction timing has clear value.

Replacing a vehicle creating maintenance costs or operational friction. Spending money keeping an old vehicle operational? Replacement decision has economic logic independent of tax timing.

The question your accountant should ask: What's the actual financial benefit of completing this transaction before 30 June versus 1 July, accounting for your specific tax position and operational requirements?

Key point: Legitimate EOFY benefits require alignment of three factors: marginal tax rate advantage, operational timing need, and threshold eligibility.

How Do Dealerships Manufacture EOFY Urgency? During EOFY sales, dealerships create urgency through specific tactics. "Low in stock." "151 items sold today." "25 people watching this item." These aren't observations. They're features designed to compress your decision timeframe.

The psychological mechanism is documented. Sales professionals manufacture urgency to prevent you from verifying claims, comparing alternatives, or consulting advisers who might reframe the decision.

Australians are expected to spend $10.5 billion during EOFY sales. Vehicle purchases represent a significant portion of this spending. The scale creates genuine stock movement, but also creates cover for artificial scarcity claims.

The structural test: If the deal is genuinely advantageous on 29 June, it should be advantageous on 2 July. If the value proposition collapses when the financial year turns over, you're responding to sales pressure, not tax timing.

The question your accountant should ask: If we completed this transaction on 2 July instead of 29 June, what would change in terms of your tax position and total cost of ownership?

Key point: Genuine tax timing benefits survive calendar changes. Manufactured urgency doesn't.

What Finance Office Add-Ons Inflate Your Total Cost? EOFY pressure accelerates the vehicle purchase decision and every decision that follows, including finance office add-ons that inflate your total cost by thousands of dollars.

Extended warranties get upsold with markups of $1,000 or more beyond actual value. Dealerships mark up interest rates above what lenders approve, sometimes adding $2,000 to $3,000 in total interest costs. Add-ons like paint protection, security etching, or gap insurance get padded, often $1,000-plus over direct value.

Combined, a professional client sees a total financing package inflated by $8,400 or more. This isn't speculative. It's the observable pattern when you examine line-by-line breakdowns most buyers never request.

The urgency architecture works against you here. Focused on "getting it done before 30 June," you're less likely to scrutinise finance terms, question add-ons, or request time to compare lender rates independently.

The question your accountant should ask: Have you seen a complete line-by-line breakdown of the finance package, including interest rate markup, warranty costs, and all add-ons, before signing?

Key point: Time pressure in June makes you less likely to scrutinise financing terms where real cost inflation occurs.

What Questions Should Your Accountant Ask Before EOFY Purchase? If your accountant advises "get it done before EOFY" without asking these questions, the advice is incomplete:

What's your marginal tax rate this year versus next year? This determines whether accelerating the deduction has genuine value or whether you're shifting timing of an equivalent benefit.

What's your actual business usage percentage after applying the car limit? This prevents overestimating the tax benefit based on vehicle purchase price.

If trading in a business vehicle, what's the depreciation recapture amount? This reveals whether the timing urgency is real or manufactured.

What's the total cost of ownership including finance terms and add-ons? This ensures you're optimising for actual cost, not tax deduction timing.

Does operational need justify the transaction timing independent of tax? This separates genuine business requirements from tax-driven decision compression.

What would change if you completed this on 2 July instead of 29 June? This exposes whether the urgency is structural or theatrical.

Key point: These six questions distinguish legitimate tax timing from manufactured dealer pressure.

When Should You Ignore EOFY Pressure Completely? Clear scenarios where EOFY timing is irrelevant to your situation:

Not using the vehicle for business purposes. It's a personal vehicle? Tax thresholds don't apply. Only consideration is whether dealership EOFY pricing represents genuine value compared to other times.

Not in a position to claim depreciation or instant asset write-off. Your business structure doesn't permit these deductions? Tax timing is meaningless.

No clarity on specific vehicle, financing structure, and total cost. Rushing to meet an arbitrary deadline when you haven't determined requirements is poor economics regardless of tax timing.

Loss-making year or low taxable income. Not facing significant tax liability this year? Accelerating a deduction has minimal value.

Quoted an inflated price creating room for "EOFY discount." Dealership artificially elevated the starting price to make the discount appear significant? You're getting theatre, not tax timing value.

Key point: EOFY pressure is irrelevant when you have no business use, no claimable deductions, or artificially inflated pricing.

How Do You Determine If EOFY Timing Matters for Your Situation? Decision framework for evaluating EOFY timing:

Step 1: Confirm legitimate tax benefit. You have a genuine tax benefit from completing the transaction before 30 June? This requires knowing your marginal tax rate, business usage percentage, and eligibility for instant asset write-off or depreciation claims.

Step 2: Calculate actual claimable amount. Apply the car limit and business usage percentage. Get the specific number, not an estimate.

Step 3: Determine total cost of ownership. Include all finance terms and add-ons. Request a line-by-line breakdown and compare lender rates independently.

Step 4: Test the timing urgency. Ask what would change if you completed the transaction on 2 July instead of 29 June. Answer is "nothing material"? Urgency is manufactured.

Step 5: Confirm operational alignment. Vehicle meets your operational requirements, and timing aligns with genuine business need, not tax calendar pressure.

You can't complete these steps with confidence? You're not ready to act on EOFY timing, regardless of dealership suggestions.

Key point: Five-step framework separates structural tax benefits from theatrical sales pressure.

What Should You Do Next? Facing EOFY pressure and not certain whether timing benefits you? Default position should be to wait. Cost of rushing into a poorly structured transaction is higher than missing an arbitrary deadline.

Determined that EOFY timing creates legitimate value for your situation? Next step is ensuring you're not paying for that timing benefit through inflated pricing, unfavourable finance terms, or add-ons that compound into significant cost.

The tax calendar is a structural reality. Pressure to act before 30 June is often manufactured. Your accountant's role is helping you distinguish between the two. If they're not asking the questions outlined here, you're not getting the advice you need.

Frequently Asked Questions About EOFY Vehicle Purchases Does the $69,674 car limit apply to all vehicles?

No. Limit applies to passenger vehicles designed to carry fewer than nine passengers and less than one tonne of load. Commercial vehicles, utes with payload capacity exceeding one tonne, and vehicles designed for nine or more passengers are exempt.

When do I start claiming depreciation on my new vehicle?

Depreciation starts from the date you first use the vehicle for business purposes, not the purchase date. Buy on 25 June but don't use it until 5 July? Depreciation starts in the 2026-27 financial year.

What happens if I use my vehicle for both business and personal purposes?

You claim only the business use percentage. Your logbook determines this percentage. Car limit applies first, then your business use percentage applies to that capped amount.

If I trade in my business vehicle, does the trade-in value affect my tax position?

Yes. Trade-in triggers a balancing adjustment (depreciation recapture). If the trade-in value exceeds the vehicle's written-down value, the difference is assessable income. If below, the difference is a deduction. Both appear on the same tax return as your new vehicle deductions.

Is the instant asset write-off better than standard depreciation?

It depends on your business structure and the vehicle cost. Instant asset write-off applies to vehicles under $20,000 for eligible businesses (turnover under $10 million). For passenger vehicles, the $69,674 car limit still applies, meaning instant write-off rarely benefits vehicles above this threshold.

Do electric vehicles get special depreciation treatment?

No. Electric vehicles are subject to the same $69,674 car depreciation limit if they qualify as passenger vehicles. Some states offer stamp duty reductions or registration benefits, but these don't change the depreciation cap.

What if the dealership inflated the price before offering an EOFY discount?

Check market pricing independently using RedBook, Glass's Guide, or comparable dealership quotes. If the pre-discount price sits significantly above market value, the EOFY discount is theatrical, not genuine value.

When should I complete the transaction to claim the deduction this financial year?

Vehicle must be purchased and first used (or installed ready for use) before 30 June 2026 to claim the deduction in the 2025-26 financial year. Purchase alone isn't sufficient. Vehicle must be operationally available for business use before 30 June.

Key Takeaways The car depreciation limit for 2025-26 is $69,674, regardless of purchase price. Maximum GST credit is $6,334.

Instant asset write-off is $20,000 (extended to 30 June 2026, now law), but the car limit still applies to passenger vehicles.

Tax benefit calculations follow a sequence: car limit first, then business usage percentage, then depreciation method. Most buyers reverse this and overestimate their deduction.

Trading in a business vehicle triggers depreciation recapture that appears on the same tax return as new deductions, often eliminating timing advantages dealers claim.

Legitimate EOFY timing benefits require three factors: marginal tax rate advantage this year, operational timing need, and threshold eligibility.

Dealerships manufacture urgency through artificial scarcity tactics. Test this by asking what changes if you complete the transaction on 2 July instead of 29 June.

EOFY pressure accelerates finance office decisions where real cost inflation occurs: extended warranties, interest rate markups, and add-ons often total $8,400 or more in unnecessary costs.

We handle vehicle acquisition for professionals who value clarity over theatre. If you're looking at an EOFY purchase and you want someone to verify whether the timing actually serves you, send through the details. We'll tell you what matters and what doesn't.