Car Finance Calculator Australia 2026 See the real cost of a car loan before you sign anything Most buyers do not get caught out by the car. They get caught out by the finance structure.

It usually looks like this.

You focus on the weekly or monthly repayment. Someone adjusts the term, tweaks the deposit assumption, adds a balloon, and the repayment drops. It feels like progress.

Then later you notice what actually mattered.

The total cost is thousands higher than you assumed. The balloon is bigger than you are comfortable clearing. The “drive-away” figure you compared was not a like for like comparison. A refinance “saving” reduced repayments but extended the debt timeline and increased total interest. If you are buying through a business, the GST effect was misunderstood or oversimplified. Carmada’s Three-in-One Car Finance Calculator is built to prevent that. It is designed for the decisions Australians actually make when comparing car finance and car loans.

Try it here → [Start here ]

Why most car finance and car loan calculators are not enough Most online tools are repayment calculators. They answer one narrow question.

“What is the repayment?”

That is a useful starting point. It is also where people get misled, because repayment can be made to look good while the overall deal gets worse.

Common gaps in basic calculators:

No stamp duty by state, so the “total” is incomplete. No visibility of registration and compulsory insurance allowances, so ownership costs are understated. No Luxury Car Tax handling, so higher priced vehicles can be mis-modelled. No balloon modelling emphasis, so buyers miss end-of-term risk. No refinance comparison across remaining cost, so “lower rate” decisions get made blindly. No side by side comparison, so people rely on memory, screenshots, and gut feel. No business-use GST estimate, so ABN purchases get treated like personal purchases. Carmada’s calculator is built as a decision tool. It helps you test scenarios quickly and see the full structure, not just the repayment.

What makes Carmada’s calculator different It is built for quick scenario testing on mobile and desktop, because that is how people actually shop and compare.

Sliders for fast what-if testing Direct number entry for precision Live recalculation on every change Plain-English prompts to reduce finance jargon Clear outputs that focus on total cost and interest, not just the monthly figure Side by side comparison built in, so you can make a clean call This is the practical advantage. You can pressure-test the deal before you are in a high-pressure conversation.

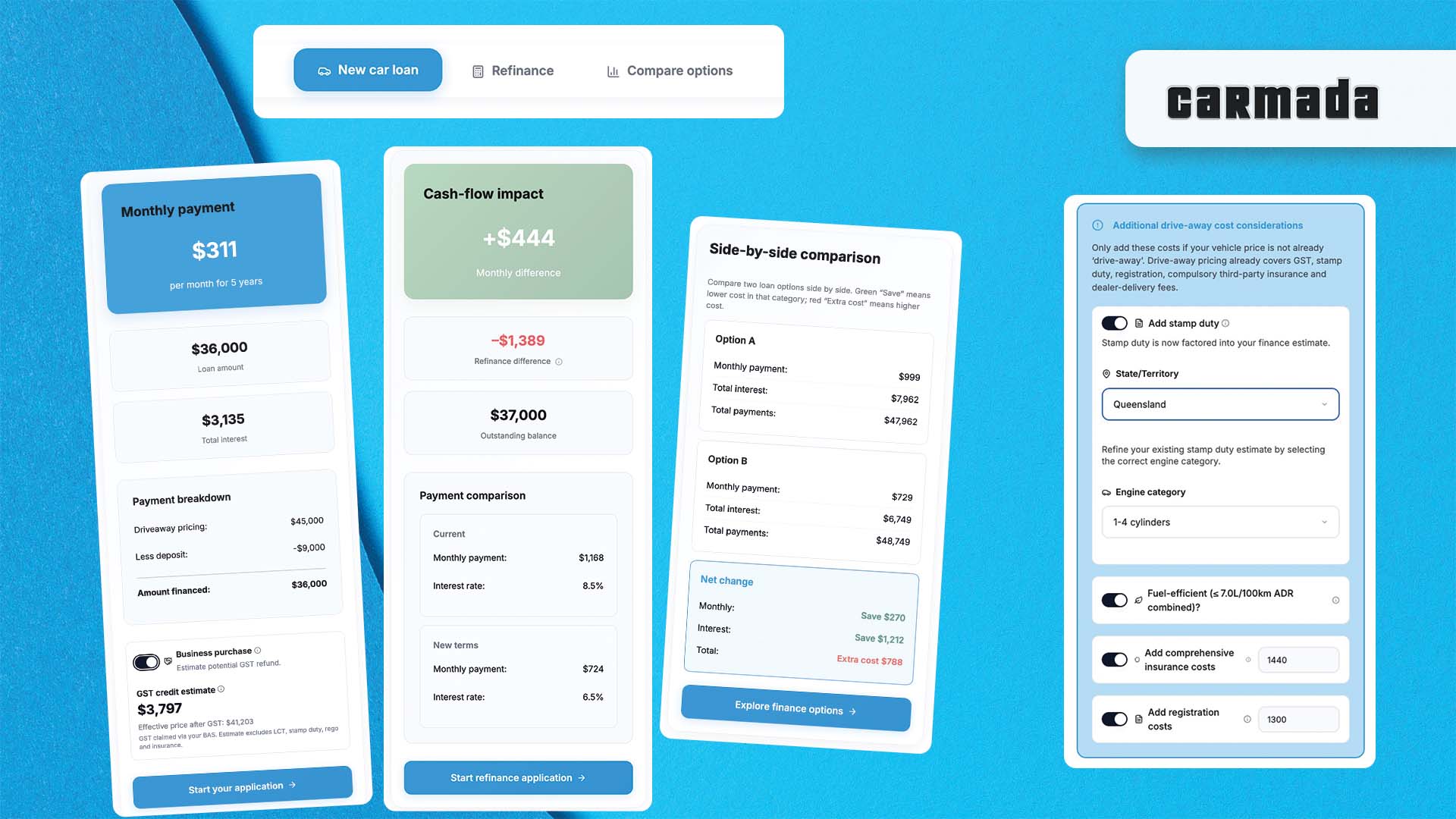

Three modes for the three decisions people actually make 1) New Car Finance Calculator “What will this car cost me in the real world?” This mode helps you model a purchase properly.

You can adjust:

Vehicle price Deposit Trade-in value Interest rate Loan term Balloon payment You can also model common real-world costs and tax factors:

Drive-away pricing on or off Stamp duty treatment by state Registration and CTP estimate Insurance estimate Luxury Car Tax threshold handling, including fuel-efficient support Business-use GST estimate with adjustable business-use percentage You see outputs that help you decide, not just browse:

Estimated repayment Total loan amount Total interest over the term Total repayments Effective cost after business GST impact (estimate) Example 1: The balloon that makes the deal look “cheap” You are shown two structures on the same car.

Option A has a lower repayment because the balloon is larger. Option B has a higher repayment because the balloon is smaller. If you choose based on repayment alone, Option A often wins emotionally. Option B often wins financially and with less end-of-term risk.

Use the balloon control, then look at total repayments, total interest, and what you still owe at the end.

Example 2: Drive-away vs not drive-away comparisons You are comparing two adverts.

Offer 1 looks cheaper, but it is not drive-away. Offer 2 looks higher, but it includes on-road costs. A repayment-only comparison can push you toward the wrong option. Toggle drive-away on or off so you can compare like for like, then compare total loan amount and total repayments.

Example 3: Deposit size versus keeping cash You can afford a larger deposit, but you are deciding whether to keep cash available.

Run two scenarios:

Bigger deposit, smaller loan, lower interest cost Smaller deposit, larger loan, higher interest cost, more cash retained This is how financially careful buyers think. It is not “how low can I push the repayment”. It is “what is the total cost, and what risk am I taking by tying up cash”.

Example 4: Business use percentage changes the picture If you are purchasing through a business, the GST impact can change the effective cost.

Run scenarios at different business-use percentages so you can see how the estimate moves. This helps you plan realistically before you commit.

Try the New Car Finance mode → [Start here]

2) Refinance Calculator “Will refinancing improve my position, or just reshuffle the timeline?” Refinancing can be a genuine win. It can also be a hidden loss if you only look at the new repayment.

This mode lets you enter your current position:

Current balance or amount owing Current rate Original term Months elapsed Balloon amount if applicable Then model the new proposal:

New rate New term New balloon if applicable Fees and setup costs You see the comparison that matters:

Current vs new repayment Monthly cash-flow impact Remaining total cost comparison Fee impact on savings Example 1: Lower rate, longer term, higher total interest You refinance to a lower rate but extend the term.

Repayments drop Total interest can increase Fees can wipe out the gain Model the refinance fees and compare remaining total cost. If the break-even period is too long, the deal is often not worth it.

Example 2: Refinancing halfway through a loan You took a five-year loan and you are partway through. A refinance offer looks attractive.

If the refinance resets you into a fresh long term, you may be turning a short remaining window into years of extra interest. Use the months elapsed input and compare what you will pay from today onwards under each option.

Example 3: Balloon risk management If your current loan ends with a balloon you do not want to face again, model a refinance structure that reduces or removes it. Then compare the repayment increase against the risk reduction.

Try the Refinance mode → [Start here]

3) Compare Car Loan Options Side by Side “Which offer is actually better?” This is for comparing two finance options properly in one place.

Option A vs Option B.

You can adjust for each:

Vehicle price Deposit Rate Term Balloon You instantly see:

Monthly repayment Total repayments Total interest The purpose is simple. It removes memory, bias, and sales framing.

Example 1: A cheaper car with a worse loan Sometimes the car price is better in one offer, but the rate and term are worse. Compare the full outcome, not a single headline number.

Example 2: Two rates that look close A small rate difference can matter materially over years. Compare total interest, then decide whether the cheaper deal is worth the extra conditions or fees attached.

Example 3: The “same repayment” illusion Two offers can be engineered to show a similar repayment by changing balloon and term. Compare total repayments and what remains owing at the end to reveal which one is truly cheaper.

Try Compare mode → [Start here]

Built for Australian conditions Many tools are generic. Australian buying decisions are not.

Carmada’s calculator is designed to reflect local factors such as:

State-based stamp duty treatment Queensland duty behaviour by engine category Luxury Car Tax thresholds including fuel-efficient handling Business-use GST estimate modelling aligned with how buyers think about BAS Registration and insurance estimates to better reflect ownership costs This is not about perfect prediction. It is about avoiding the big structural mistakes that basic calculators miss.

Who this is for This tool is designed for buyers who want clarity before they commit.

Private buyers upgrading a car or ute ABN and business buyers modelling GST impact People comparing two lenders or two deal structures Anyone considering refinancing and wanting a clean answer Time-poor buyers who want to run the numbers quickly before a conversation If you prefer being informed and in control, this tool supports that.

What the calculator does not do It does not replace lender assessment or a formal quote.

Final numbers can vary due to:

Your credit profile and personal details Lender approval criteria Dealer fees and inclusions Insurance provider quotes The calculator gives structured estimates so you can make better decisions earlier, with fewer surprises later.

Frequently asked questions Is this car finance calculator accurate for Australia? It is designed around Australian conditions and uses structured duty and tax logic. Outputs are estimates based on your inputs. Final figures depend on lender approval and personal circumstances.

Does it include stamp duty and Luxury Car Tax? Yes. It models state-based stamp duty and Luxury Car Tax thresholds, including fuel-efficient handling.

Can I use it for a business purchase through my ABN? Yes. You can adjust business-use percentage and see an estimated GST impact.

Can I compare two car loans side by side? Yes. Compare mode runs two scenarios at once and shows repayment, total repayments, and total interest.

Can it help me decide whether to refinance? Yes. Refinance mode compares current versus proposed terms, including fees, and shows whether the move improves your position.

Use it properly in under two minutes Run the scenario you are leaning toward. Stress-test it by changing one variable at a time, especially term and balloon. When comparing offers, look at total interest and total repayments before you look at the repayment. Try it now → [Start here ]

Secondary option if you want a human check on the structure:Talk to Carmada ]