TL;DR: When the RBA changes interest rates, the biggest impact on car finance happens within 72 hours—before advertised rates change. Lenders immediately adjust serviceability buffers, credit score requirements, and LVR limits, which determines who gets approved and at what terms. Loan structure (term length, balloon payments, exit flexibility) matters more than advertised rates for total cost. The 10–30 day window after RBA signals creates optimal buying opportunities before the market reprices.

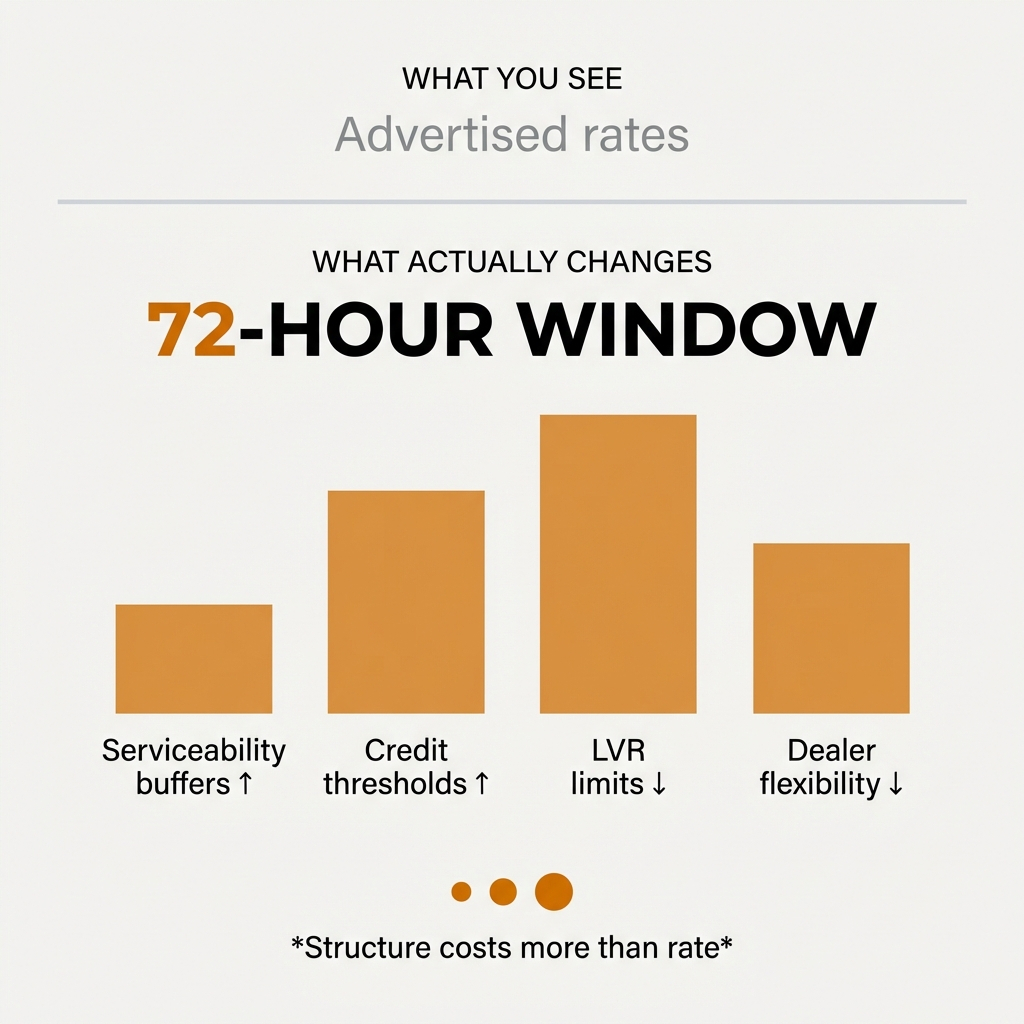

Invisible changes happen first: Lenders adjust approval criteria 72 hours after RBA decisions, tightening serviceability buffers (testing repayments at 2–3% above loan rates), raising credit score thresholds (e.g., 850+ to 900+ on Equifax), and reducing LVR limits (95% to 90%).Structure costs more than rate: A 5.99% loan with mandatory balloon and 5-year cap can cost more than a 6.79% loan with 7-year term and clean exit—total cost difference averages $1,800–$3,200.Comparison rates mislead: They assume perfect credit, fixed loan structure, and full-term repayment—conditions most buyers don't meet. Real cost lives in flexibility, exit paths, and approval probability.Timing creates advantage: Buy 10–30 days after easing signals (before advertised rate cuts) or avoid 2–4 weeks after tightening decisions when approval filters narrow fastest.Information asymmetry inflates cost: Traditional shopping exposes your contact details before seeing competitive quotes, costing 7–12% more on average. Sealed competitive sourcing prevents information leakage that increases prices.Why RBA Rate Decisions Change More Than Interest Rates When the RBA increased the cash rate to 3.85% in February 2026, most buyers focused on the headline number.

They checked comparison sites, calculated monthly repayments, and assumed the advertised rate was the main variable. They were optimising the wrong thing.

They were optimising the wrong thing.

The real changes happened in the 72 hours after the announcement, before any "new rate" banners appeared.

Lenders repriced their funding lines within hours. That flowed straight into approval criteria, risk tiers, and dealer finance discretion—all invisible to buyers.

Two buyers with identical credit scores suddenly got very different approvals the week after the decision, even though rates looked unchanged.

That invisible tightening is what quietly shifts buyer power long before headlines catch up.

The bottom line: Advertised rates are decoration. Approval filters are what determine who gets financed and at what true cost.

What Changes in the First 72 Hours After an RBA Decision After an RBA decision, lenders narrow the approval funnel first, then adjust pricing later.

Here's what changes whilst you're still reading analysis pieces about what the rate move "means":

1. Serviceability Buffers Tighten Immediately Lenders don't change your rate first. They change the maths behind the rate.

Lenders quietly tweak the assessment rate they use to test repayments.

Example: You're offered 7.49%, but the lender tests you at 9.99% instead of 9.49%.

Whilst car finance lenders aren't regulated by APRA like mortgage lenders, many apply similar assessment buffers—testing your repayment capacity at rates 2–3 percentage points above the actual loan rate.

That 0.5% buffer change alone can cut borrowing power by 5–8%.

A comfortable approval becomes borderline. If your deal was tight before the decision, waiting makes it worse.

Key insight: Serviceability buffer changes reduce loan amounts before any advertised rate movement occurs.

2. Credit Score Requirements Rise Overnight This is the fastest lever lenders pull.

They don't reprice everyone—they move the line that determines which tier you fall into.

A credit score that qualified for prime rates drops to near-prime overnight.

In Australia, lenders use Equifax (0–1,200), Experian (0–1,000), or Illion (0–1,000) credit scores.

What was considered excellent (say, 850+ on Equifax) might suddenly require 900+ for the same tier.

Same buyer, same profile, different bucket.

That changes your max loan amount, whether conditions apply, and whether the deal gets auto-approved or requires manual review.

This is where "why did my mate get approved and I didn't?" emails spike.

Key insight: Credit score thresholds shift before rates, changing approval outcomes for identical borrower profiles.

3. Loan-to-Value Ratio (LVR) Limits Drop LVR is a silent killer post-decision.

Max LVR drops from 95% to 90%. EVs and used cars get hit first. Certain brands get flagged as higher risk.

You don't hear about it—you just get asked for a bigger deposit.

Higher LVRs mean lenders are taking on more risk because they're lending you more relative to the car's value.

When risk appetites tighten, those limits drop fast.

Low-deposit buyers feel the pain before anyone else.

Key insight: LVR limits tighten immediately after RBA decisions, requiring larger deposits without explanation.

4. Dealer Finance Flexibility Disappears This one's invisible to you.

Lenders reduce dealer rate-buy-down flexibility, approval overrides, and "we'll make this work" exceptions.

Even if the headline rate looks the same, the dealer has less room to fix the deal.

That's why post-RBA weeks feel suddenly rigid.

Key insight: Dealer discretion evaporates after rate decisions, making approvals less flexible even at unchanged rates.

5. Loan Structure Rules Become Stricter Before rates move, structure tightens.

Max term reduced from 7 years to 6. Balloon limits lowered. Self-employed add-backs restricted.

Repayments go up without the rate changing. That's the quiet squeeze.

Key insight: Loan structure restrictions reduce affordability independently of advertised rate changes.

When to Buy: The 10–30 Day Window After RBA Easing Signals The lag between RBA signals and retail repricing is where buyers win: 10–30 days.

Funding markets move first. Lender behaviour loosens second. Advertised rates move last.

That gap is your green light.

What Loosens First (In Order) Serviceability buffers soften. Assessment rates get nudged down 0.25–0.50% before headlines change.

Borrowing power jumps 5–10%. Marginal buyers suddenly pass.

If you were "just short" last month, this is your moment.

Risk tiers widen. Lenders don't cut rates—they let more people into the top tiers.

Credit score thresholds drop. Fewer manual reviews. Cleaner auto-approvals.

Same rate, better outcome.

LVR limits creep up. 90% to 95% returns quietly.

Used cars and EVs get re-enabled. Smaller deposits get approved again.

Dealers notice before buyers do.

Dealer discretion comes back. Overrides, rate buy-downs, and "make it work" approvals reopen.

This is when two buyers get wildly different deals on the same car.

Timing Signals We Watch Not press releases.

We watch: assessment rate sheets updating, auto-approval volumes rising, declines turning into conditional approvals, and dealer callbacks speeding up.

When approvals get faster, the market is loosening.

The simple rule: Buy before the rate cut shows up on a banner.

Once it's public, competition returns and prices firm.

Key insight: The optimal buying window is 10–30 days after easing signals, before advertised rate cuts attract competition.

Why Advertised Rates Don't Determine Total Cost Here's a specific example:

A buyer chases a 5.99% advertised rate they saw online. Looks unbeatable.

Same buyer could've taken 6.79% elsewhere. They pick the 5.99%.

What the Lower Rate Actually Cost Shorter max term. The 5.99% lender caps term at 5 years. Other lender allows 7 years.

Result: higher monthly repayments, serviceability fails, loan amount reduced by $6,000.

Buyer has to stretch deposit or downgrade the car.

Mandatory balloon payment. Low rate requires a 30% balloon.

The maths looks cheap until the end. Over 5 years: lower interest paid, but a $12,000 lump sum still owing.

Buyer refinances that balloon later at 9.2%. Total cost explodes.

No early exit flexibility. They sell the car at year 3.

Break cost plus fixed structure equals $2,400 penalty.

The 6.79% loan? No break fee. No balloon.

Total Cost Comparison 5.99% loan: Higher repayments, forced balloon refinance, exit penalty.

Total cost: higher.

6.79% loan: Longer term, no balloon, clean exit.

Total cost: lower.

The rule: The advertised rate optimises interest. The structure determines total cost.

Rate is decoration. Structure is the bill.

When we audit deals, the most expensive loans are rarely the highest rates.

They're the "cheap" ones with handcuffs.

Key insight: Loan structure (term length, balloon requirements, exit flexibility) creates more cost variance than advertised rate differences.

Why Comparison Rates Mislead Car Buyers The comparison rate feels transparent but quietly lies.

It's not fraud. It's assumptions that don't match reality.

What Comparison Rates Assume (vs. Reality) Assumption 1: A fictional borrower. Perfect credit, full approval, no pricing adjustments, no dealer discretion.

Most real buyers don't match that profile. Miss it by one variable, and the comparison rate is irrelevant.

Assumption 2: A fixed loan structure. Comparison rates lock in a standard term (often 5 years), a fixed loan size, and no behaviour changes.

But real loans flex. Terms stretch or shorten. Balloons get added. Deposits vary.

Change the structure, the comparison rate breaks.

Assumption 3: Zero timing risk. It assumes you keep the loan for the full term, never refinance, never sell early.

Most car loans don't run full term. Comparison rates don't model exits—which is where real cost hides.

Assumption 4: Fees averaged, not experienced. Upfront fees, exit fees, and refinance penalties all get blended into a neat annual number.

In real life, they hit at the worst possible moment.

Assumption 5: No probability weighting. This is the killer.

Comparison rates don't ask: "What's the chance this borrower actually gets this deal?"

A 6.2% comparison rate that only 15% of applicants qualify for beats a realistic 7.1% on paper—and loses in practice.

The Core Problem with Comparison Rates Comparison rates answer: "What does this loan cost in a perfect, static world?"

You live in: changing income, changing needs, changing markets.

So you optimise the wrong thing.

The biggest blow-ups happen when buyers win the comparison-rate war and lose the real-cost one.

Rule: If a loan looks cheap only if nothing changes, it's expensive.

Real cost lives in flexibility, exit paths, and approval probability.

Comparison rates don't price those.

Key insight: Comparison rates assume perfect conditions most borrowers don't meet, making them poor predictors of actual cost.

How Dealerships Create Decision Pressure There's a moment where buyers flip from "I'll shop around" to accepting a suboptimal structure.

It's not persuasion. It's compression.

The system collapses time, options, and cognitive energy into one narrow moment.

What Happens During the Finance Decision 1. Approval becomes the emotional anchor. The moment you hear "you're approved", the goal shifts.

You didn't come to buy a loan. You came to remove uncertainty.

Once approval lands, your brain flips from "What's optimal?" to "Don't lose this."

2. Structure is framed as immovable. Rates feel negotiable. Structure doesn't.

Phrases like "That's just how this lender does it" or "All approvals look like this right now" aren't lies.

They're contextual truths used at the exact moment resistance is lowest.

3. Optionality is quietly removed. The real pressure mechanism is fatigue.

By the time structure is discussed, you've picked the car, visualised ownership, invested time, and mentally spent the money.

Shopping around now means starting again. So "I'll compare later" turns into "This is probably fine."

4. Monthly repayment framing overrides total cost. The decision collapses into one number.

If the repayment fits the weekly budget, the structure passes.

Balloon? Term? Exit cost? Those are future problems. The system knows buyers discount the future at 30–40% under pressure.

5. Scarcity is real, not fake. Approvals do expire. Cars do sell. Policy windows do close.

So urgency isn't invented—it's selectively emphasised. That makes hesitation feel risky.

When Decision Quality Collapses It's when you think: "I don't want to mess this up."

At that point, certainty beats optimisation.

The biggest unlock wasn't better rates—it was giving buyers space after approval, before commitment.

That's where bad structures usually sneak in.

Rule: If a decision is rushed after approval, structure suffers.

Good loans survive daylight. Bad ones need momentum.

Key insight: Decision compression after approval causes buyers to accept suboptimal structures they would reject with time to analyse.

When Paying Cash Costs More Than Financing Most advice says "if you can pay cash, pay cash."

But paying cash costs more when your capital has a higher job to do than "avoid interest."

That flip happens in three specific scenarios:

Scenario 1: When Liquidity Has Option Value Car price: $60k. Finance: 6.5% all-in. Cash alternative: offset account saving you roughly 6% after tax.

On paper, cash "wins."

But if that $60k keeps you liquid, prevents redraw risk, and avoids selling assets later, the option value alone can beat the interest saved.

Decision rule: If paying cash reduces flexibility, you're underpricing its cost.

Scenario 2: When Cash Forces Asset Downgrade This is where advice breaks.

Cash buyers anchor on "what feels reasonable today." Financed buyers can optimise total lifecycle cost.

Real example: Cash buyer drops from a $70k car to $55k to stay "comfortable."

Ends up with higher depreciation percentage, shorter ownership cycle, and earlier replacement.

They save $15k upfront and lose it back in 3–4 years.

Decision rule: If cash forces you into a worse asset, it's not cheaper—it's constrained.

Scenario 3: When Income Is Volatile This hits founders, contractors, and anyone with lumpy income.

Paying cash drains buffers, increases downside risk, and forces bad decisions later (selling assets, refinancing under pressure).

Financing spreads risk over time—which has real economic value.

Early users who regretted cash purchases all had the same story: "I didn't need the money… until I did."

Five Variables That Determine Cash vs. Finance Not ideology. These five inputs:

Cost of capital (real, after tax)Liquidity value (what cash protects you from)Asset quality change (what car choice cash forces)Income volatility (how predictable your future cash is)Exit flexibility (can you unwind without penalties?)Ignore any one of these and "pay cash" becomes lazy advice.

Internal rule: If cash improves certainty without reducing optionality, use it.

If it reduces optionality, finance—even at a higher headline cost.

Interest is visible. Constraint is not.

Key insight: Cash has opportunity cost beyond interest savings—liquidity value, asset quality decisions, and risk distribution often outweigh nominal interest costs.

How Information Asymmetry Inflates Car Finance Costs Traditional car finance shopping works like this:

You walk into a dealership or fill out an online form. Your contact details become leverage currency.

Within hours, you're fielding calls from multiple lenders and dealers, each trying to position their offer as competitive whilst lacking visibility into what others are actually quoting.

You're trying to create competition, but you've already lost the structural advantage.

Information flows one way—from you to them.

They know your urgency, your budget ceiling, your approval status.

You don't know their true floor price, their dealer incentives, or which lender is actually hungry for your profile this week.

What Changes with Sealed Competitive Sourcing When the buyer remains anonymous until commitment, three structural variables shift:

1. Pricing discipline returns. Dealers and lenders can't anchor on "what this buyer will accept."

They have to quote their genuine competitive position because they don't know if they're bidding against two competitors or five.

The spread between "opening offer" and "actual floor" collapses.

2. Structure becomes negotiable. Without knowing your approval status or urgency level, lenders can't selectively tighten terms.

Balloon requirements, term flexibility, and early exit clauses get priced transparently because they can't gauge your tolerance for constraints.

3. Time pressure reverses. In traditional shopping, urgency works against you.

Lenders know when approvals expire. Dealers know when you've emotionally committed to a car.

In sealed sourcing, urgency works for you—lenders compete on speed because they don't know if you're comparing them simultaneously or sequentially.

Cost Impact of Information Asymmetry Across transactions we've handled, the variance between "first offer" and "final competitive price" averages 7–12% on the vehicle.

Structure improvements (term flexibility, removal of balloons, exit clause additions) that would cost $1,800–$3,200 to negotiate separately come standard.

That's not because we're better negotiators.

It's because the architecture prevents information leakage that normally inflates cost.

Why This Matters When Rates Rise When rates are climbing, lenders get selective about which deals they want.

They don't broadcast this—they just quietly tighten approvals for profiles that don't fit their current book.

If you're shopping traditionally, you waste time with lenders who were never going to approve you competitively.

You don't know which lender currently favours your employment type, your deposit level, or your vehicle choice until after you've exposed your details.

Sealed sourcing flips this.

Lenders self-select based on genuine appetite. The ones who respond are the ones who actually want your business at that moment.

You're not trying to convince a reluctant lender—you're choosing between genuinely interested ones.

Structural rule: Information asymmetry inflates cost in two ways—through pricing opacity and through wasted time with mismatched lenders.

Remove both, and the finance equation changes before you even discuss rates.

Key insight: Protecting buyer information until commitment reduces total costs by 7–12% on average because lenders can't anchor pricing on buyer urgency or alternatives.

What to Do Before Your Next Car Purchase The RBA's February 2026 decision wasn't just a rate move. It was a signal that the loosening cycle has ended.

NAB is forecasting another hike in May 2026, which would bring the cash rate to 4.10%.

If you're planning to buy in the next 6–12 months, the window for optimal structure is narrowing.

Not because rates are rising—that's the headline.

Because approval architecture is tightening, and most buyers won't notice until they're sitting in a dealership wondering why their mate got better terms last month.

Three Variables That Matter More Than Rate 1. Timing relative to policy lag. Buy in the 10–30 day window after signals of easing, before repricing.

Avoid the 2–4 weeks after tightening decisions, when filters narrow before rates move.

2. Structure over advertised rate. A 6.8% loan with no balloon, 7-year term, and clean exit beats a 5.9% loan with mandatory balloon, 5-year cap, and exit penalties.

Total cost lives in structure, not headline rate.

3. Information architecture. If your shopping process requires exposing contact details before seeing competitive quotes, you've already paid a premium.

The cost of information asymmetry exceeds the cost of most rate differences.

The next RBA decision will move rates. But the real changes happen in the 72 hours after, in systems most buyers never see.

If you're optimising for advertised rates, you're solving the wrong equation.

Structure determines cost. Timing determines approval. Information architecture determines leverage.

Everything else is noise.

Frequently Asked Questions How long after an RBA rate decision should I wait to apply for car finance? Don't wait after a rate increase—apply before if possible, as approval criteria tighten within 72 hours. After a rate decrease or easing signal, the optimal window is 10–30 days later, before advertised rates drop and competition increases. This is when serviceability buffers soften and credit score thresholds widen, but before the market reprices publicly.

What credit score do I need for car finance in Australia in 2026? Australia uses three credit bureaus: Equifax (0–1,200), Experian (0–1,000), and Illion (0–1,000). Requirements vary by lender, but generally 661+ on Equifax, 625+ on Experian, or 500+ on Illion qualifies as "good." After RBA tightening decisions, thresholds can jump (e.g., from 850+ to 900+ on Equifax for prime rates). The tier you fall into matters more than your absolute score because it determines loan amount, conditions, and whether you get auto-approved.

Is a 5.99% car loan always better than a 6.79% car loan? No. The 5.99% loan might have a shorter maximum term (5 years vs. 7 years), mandatory balloon payment (30% owing at the end), and exit penalties ($2,400+). These structural constraints can make total cost higher despite the lower rate. A 6.79% loan with longer term, no balloon, and clean exit typically costs less over the life of the loan. Structure determines total cost more than advertised rate.

Why do comparison rates not reflect my actual car loan cost? Comparison rates assume: perfect credit, fixed 5-year term, no early exit, and that you qualify for the advertised rate. Most buyers don't meet all these conditions. They don't account for balloon payments, term changes, or the probability you'll actually receive that rate. Real cost lives in flexibility, exit clauses, and approval probability—none of which comparison rates measure. If only 15% of applicants qualify for a "6.2% comparison rate," it's misleading for the other 85%.

What is LVR and why does it matter for car loans? Loan-to-Value Ratio (LVR) is how much you're borrowing relative to the car's value. A $57,000 loan on a $60,000 car is 95% LVR. After RBA decisions, lenders often drop maximum LVR from 95% to 90%, requiring larger deposits (from $3,000 to $6,000 in this example). Higher LVRs mean lenders take on more risk, so limits tighten when rates rise. Low-deposit buyers are affected first and fastest.

Should I pay cash for a car or finance it? It depends on five variables: (1) cost of capital (real, after tax), (2) liquidity value (what cash protects you from), (3) asset quality (whether cash forces you into a worse car), (4) income volatility (how predictable your cash flow is), and (5) exit flexibility. If cash reduces your flexibility, drains emergency buffers, or forces you into a lower-quality asset that depreciates faster, financing can cost less despite interest payments. Cash has opportunity cost beyond interest savings.

How does sealed competitive sourcing reduce car finance costs? When your information remains private until commitment, lenders can't anchor pricing on your urgency, budget, or alternatives. They must quote genuine competitive positions because they don't know if they're competing against two or five other lenders. This collapses the spread between "opening offer" and "actual floor"—averaging 7–12% lower vehicle prices and $1,800–$3,200 in structure improvements (term flexibility, no balloons, exit clauses). Information asymmetry inflates cost through pricing opacity and wasted time with mismatched lenders.

What happens to dealer finance flexibility after RBA decisions? Lenders reduce dealer discretion immediately after RBA decisions. Dealers lose rate-buy-down flexibility, approval overrides, and "we'll make this work" exceptions. Even if advertised rates look unchanged, dealers have less room to adjust terms or fix borderline deals. This is why post-RBA weeks feel rigid—structural flexibility disappears before rate changes become visible. When rates ease, this flexibility gradually returns over 10–30 days.

Key Takeaways Approval criteria change 72 hours before rates: After RBA decisions, lenders immediately adjust serviceability buffers, credit score thresholds, and LVR limits—determining who gets approved before any advertised rate changes appear.Loan structure costs more than advertised rate: Term length, balloon payments, and exit flexibility create $1,800–$3,200+ in cost variance—often exceeding the impact of a 0.8% rate difference.Comparison rates assume perfect conditions: They model fictional borrowers with perfect credit, fixed terms, and full-term repayment—conditions most buyers don't meet, making them poor predictors of actual cost.Timing creates 10–30 day buying windows: Buy after easing signals but before advertised rate cuts (when approval criteria loosen but competition hasn't returned) or avoid 2–4 weeks after tightening decisions when filters narrow fastest.Information exposure costs 7–12% on average: Traditional shopping exposes your urgency and alternatives before you see competitive quotes, allowing lenders to anchor pricing higher. Sealed sourcing prevents this information leakage.Cash has hidden opportunity costs: Beyond interest savings, cash decisions affect liquidity buffers, asset quality choices, and risk distribution—often making financing cheaper despite nominal interest costs.RBA signals matter more than headlines: The real impact happens in invisible approval architecture (buffers, tiers, LVR limits) within 72 hours, not in advertised rates that change weeks later.